Could saving more down payment Cost you?

Sure, who could argue that more down payment isn't better when buying a home? But can you save faster than mortgage interest rates climb?

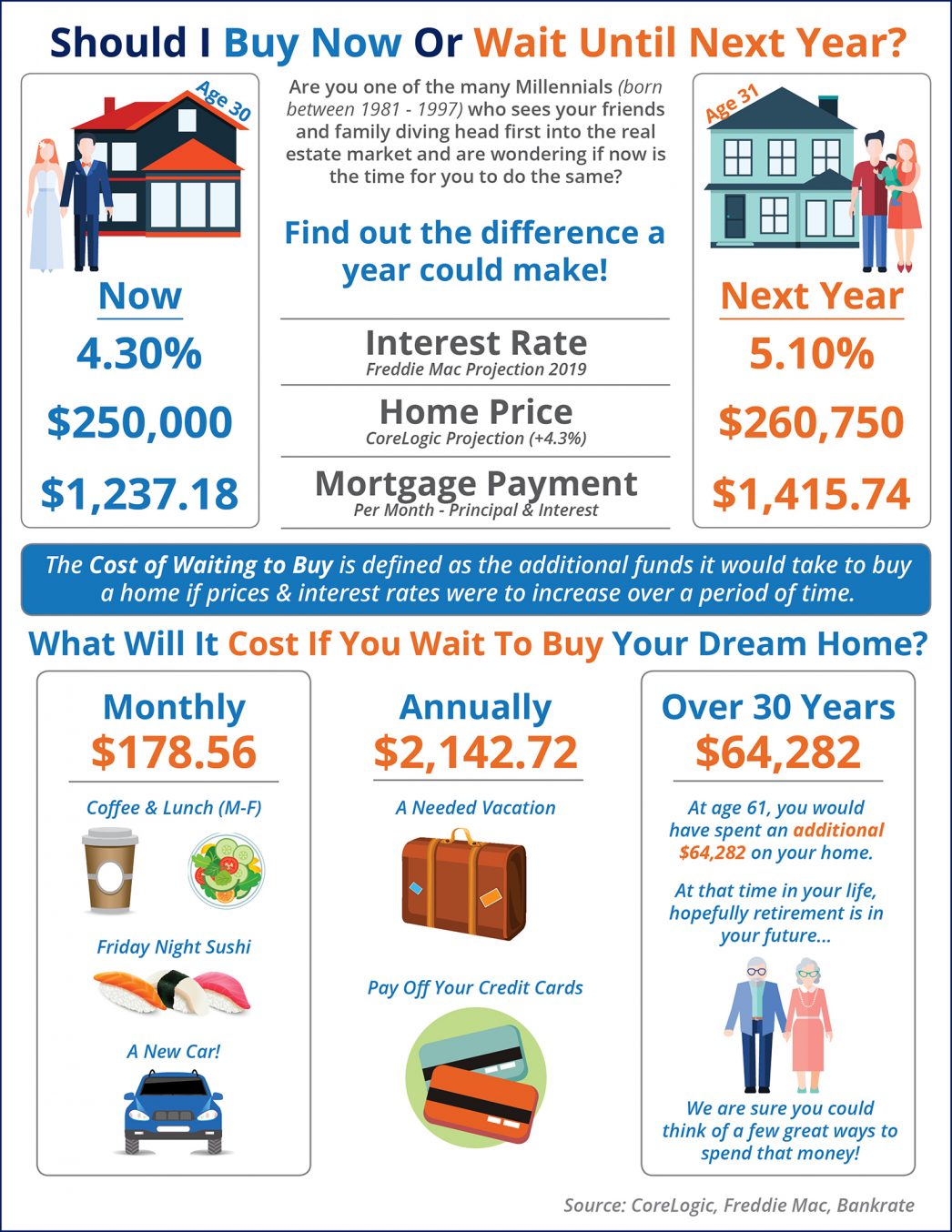

Say you can buy a $250,000 home today with your current savings. Your payment is around $1237. But you want to save another $10,000 and drop that payment down some...so you wait...and save. Maybe you can save $800-$850 a month. Meanwhile, interest rates continue their slow climb. A year later, you have the extra $10,000 to put down, but wait...now interest rates have gone up...and so have home prices! Your new payment for the same house isn't lower at all-it's actually...Higher!

Whaaat?!

Look at this graphic to see how it works.

So after a year of hard saving, instead of getting a lower house payment, you end up paying even MORE! And now, maybe you wish that you'd made your move when the rates were lower and prices were better. The rates aren't likely to ever go back down to the crazy-low levels we saw a few years ago. And the attraction of real estate as an investment is that the values go UP over time-not down.

When asked, "What is the best time to buy a home?" a lot of real estate professionals answer "Today!". That's not a sales pitch or a pressure tactic folks-it's just plain true. The market we've been in for the last several years might best be termed an anomaly-based on some very specific, economic and political factors-not based on history. While the typical real estate market will always ebb & flow, on the whole interest rates and property values tend to move North. So don't be afraid to get out there and see what your money will buy today. There are also some great programs out there for buyers who meet income and household size guidelines to qualify for assistance on the lines of low/no interest loans, deferred repayment loans and forgivable grants. Talk to Glenn or your favorite real estate professional to learn more. And do it today.